Introduction

Nigeria’s credit ecosystem is rapidly expanding, driven by fintech growth, digital lending, and regulatory enforcement of credit reporting standards. At the centre of this ecosystem are credit bureaus; institutions licensed to collect, analyse, and distribute credit information on individuals and businesses.

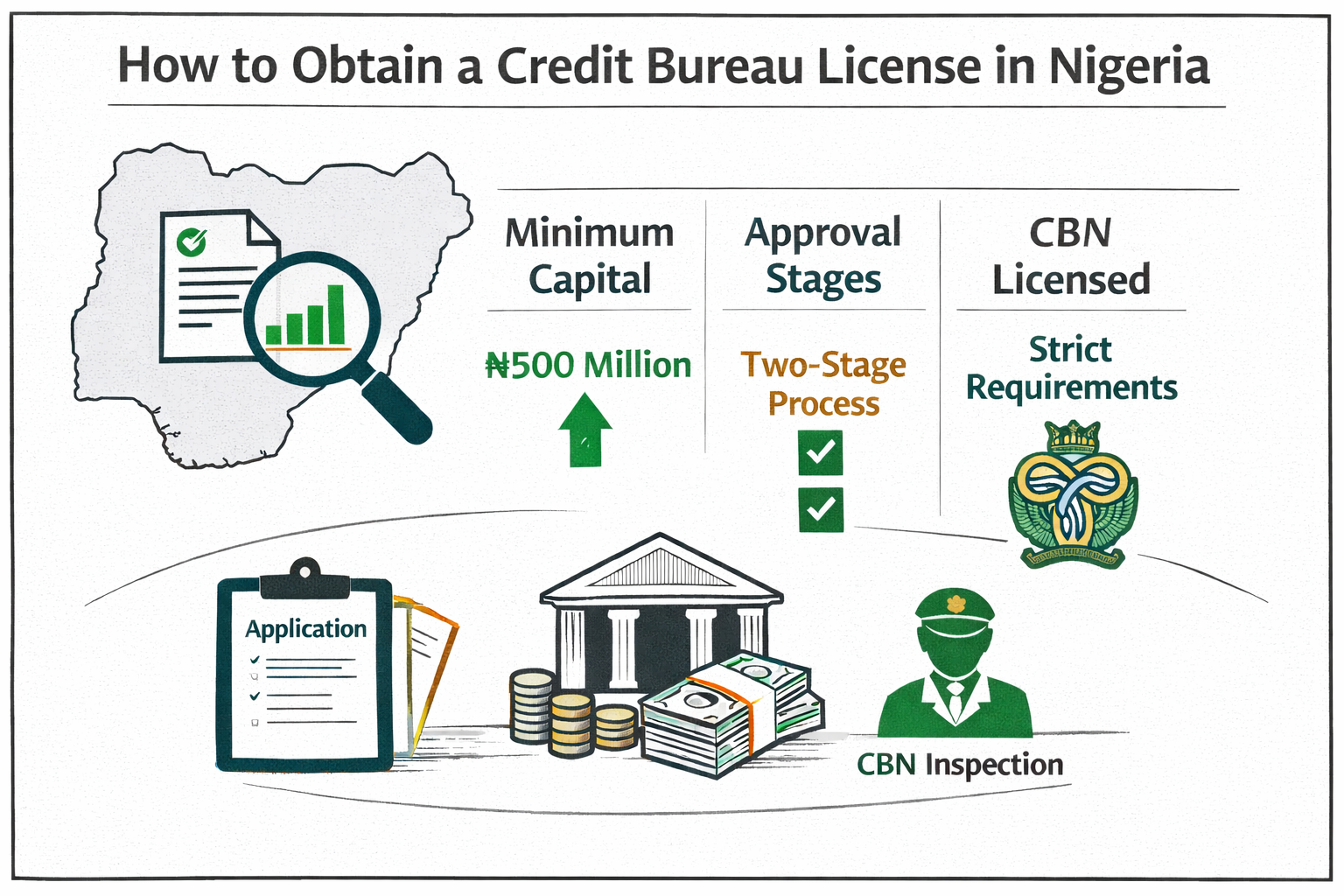

Under Nigerian law, no entity can operate as a credit bureau without a license from the Central Bank of Nigeria (CBN).

This guide provides a comprehensive breakdown of:

- Legal framework

- Requirements

- Costs

- Step-by-step process

- Documentation

- Approval timelines

- FAQs & misconceptions

All information is derived strictly from official regulatory sources such as CBN guidelines and the Credit Reporting Act.

1. Regulatory Authority for Credit Bureau Licensing in Nigeria

The sole regulator responsible for licensing credit bureaus in Nigeria is:

- Central Bank of Nigeria

Legal Framework Governing Credit Bureau Licensing

| Law / Regulation | Purpose |

|---|---|

| Credit Reporting Act 2017 | Governs credit reporting ecosystem |

| CBN Act 2007 | Empowers CBN to license financial institutions |

| CBN Guidelines for Licensing Credit Bureaux | Operational and licensing framework |

The law clearly states:

A person shall not operate as a credit bureau unless licensed by the CBN.

2. What is a Credit Bureau?

A credit bureau is a licensed institution that:

- Collects credit data from lenders and public sources

- Generates credit reports and scores

- Supplies credit information to lenders

These institutions play a critical role in Nigeria’s financial system, as banks are required to obtain credit reports before granting loans.

3. Types of Credit Bureau Licenses in Nigeria

The CBN does not classify credit bureau licenses into multiple tiers like banking licenses. Instead, there is a single unified license, but with strict operational scope and compliance obligations.

4. Minimum Capital Requirement

One of the most critical entry barriers is the capital requirement.

CBN Capital Requirement Table

| Requirement | Amount |

|---|---|

| Minimum Paid-up Capital | ₦500,000,000 |

| Deposit Structure | 50% refundable deposit with CBN |

- The capital must be paid-up and verifiable

- Evidence of deposit must be submitted with the application

5. Key Requirements for Credit Bureau License

Below is a complete breakdown of requirements based strictly on CBN guidelines.

5.1 Corporate Requirements

- Company must be incorporated in Nigeria

- Registered with Corporate Affairs Commission (CAC)

- Clearly defined ownership structure

5.2 Governance Requirements

- Board of Directors with proven integrity

- Experienced management team

- Defined organisational structure

5.3 Technical Requirements

- Data processing infrastructure

- Credit reporting systems

- IT security framework

- Data protection compliance

5.4 Financial Requirements

- Evidence of capital deposit

- Source of funds verification

- Financial projections

5.5 Operational Requirements

- Business plan / feasibility report

- Risk management framework

- Internal control policies

6. Required Documents (Full Checklist)

Below is a comprehensive document checklist required by the CBN:

Corporate Documents

- Certificate of Incorporation

- Memorandum & Articles of Association

- CAC Forms or Status report

Financial Documents

- Evidence of capital deposit

- Bank statements

- Source of funds declaration

Management & Governance

- CVs of directors and key officers

- Means of identification

- References

Technical & Operational

- Business plan

- IT architecture plan

- Data protection policy

- Risk management framework

Other Documents

- Tax clearance certificates

- Shareholding structure

- Legal compliance documents

7. Step-by-Step Process to Obtain Credit Bureau License

The licensing process follows a two-stage approval system.

Stage 1: Application for Approval-in-Principle (AIP)

Step 1: Prepare Application

- Address application to the Governor of CBN

- Include all required documents

Step 2: Pay Application Fee

- (CBN typically prescribes a non-refundable fee)

Step 3: Submit Application

- Submit to Banking Supervision Department

Step 4: CBN Review

- Due diligence on promoters

- Verification of capital

Step 5: Grant of Approval-in-Principle (AIP)

- Issued if requirements are satisfied

Stage 2: Final License Approval

Step 6: Incorporate Company

- Complete CAC registration

Step 7: Set Up Infrastructure

- Office space

- IT systems

- Staff recruitment

Step 8: Submit Final Documents

- Evidence of operational readiness

Step 9: CBN Inspection

- Physical inspection of facilities

Step 10: Grant of Final License

- Full authorisation to operate

8. Licensing Costs Breakdown

| Cost Component | Amount |

|---|---|

| Minimum Capital | ₦500,000,000 |

| Application Fee | Prescribed by CBN |

| Licensing Fee | Prescribed by CBN |

| Legal & Consulting Fees | Variable |

Note: The capital deposit is refundable subject to conditions.

9. Timeline for Approval

| Stage | Timeline |

|---|---|

| Application Review | 90 days |

| AIP to Final License | Up to 6 months |

CBN typically communicates decisions within 90 days of submission.

10. Compliance Obligations After Licensing

Once licensed, credit bureaus must:

- Ensure data accuracy

- Protect consumer information

- Maintain confidentiality

- Submit periodic reports to CBN

The Credit Reporting Act imposes strict obligations on data handling and consumer rights.

11. Role of Credit Bureaus in Nigeria’s Financial System

Credit bureaus are essential because:

- Banks must obtain credit reports before lending

- They reduce loan default risk

- Improve financial inclusion

- Support fintech lending

12. Common Mistakes Applicants Make

- Underestimating capital requirements

- Weak business plans

- Poor governance structure

- Inadequate IT infrastructure

- Non-compliance with data protection laws

13. Frequently Asked Questions (People Also Ask)

1. Who issues credit bureau licenses in Nigeria?

The Central Bank of Nigeria (CBN).

2. What is the minimum capital requirement?

₦500 million.

3. Can a foreign company own a credit bureau?

Yes, but it must be incorporated in Nigeria.

4. How long does the process take?

Typically 3–6 months.

5. Is the capital refundable?

Yes, subject to regulatory conditions.

6. Do fintech companies need a credit bureau license?

Only if they intend to operate as a credit bureau.

14. Common Misconceptions

Misconception 1: “Company registration is enough”

False. A CBN license is mandatory.

Misconception 2: “Credit bureaus are optional”

False. Banks must use them before lending.

Misconception 3: “Capital can be pledged later”

False. Capital must be deposited upfront.

15. Strategic Considerations Before Applying

Before proceeding, investors should consider:

- High capital requirement

- Regulatory scrutiny

- Technical infrastructure cost

- Data protection obligations

16. Conclusion

Obtaining a Credit Bureau License in Nigeria is a highly regulated, capital-intensive process governed by the Central Bank of Nigeria and the Credit Reporting Act.

To succeed, applicants must:

- Meet the ₦500 million capital requirement

- Provide robust documentation

- Demonstrate technical and governance capacity

- Pass CBN’s two-stage approval process

With the rise of fintech and digital lending, credit bureaus remain one of the most strategic licenses in Nigeria’s financial sector.